I regularly ask my Instagram followers to choose the subject for my next analysis article. Those articles have gotten a lot of positive feedback so I’m happy to keep publishing them. It also gives me good insight into which stocks are on most investors radar. The latest requested dividend stock analysis will be about Coca-Cola(KO)

Check out previously requested articles on Visa(V), on AT&T(T) and the latest article on Procter&Gamble(PG).

Click here to see my own personal dividend portfolio.

Coca-Cola Company(KO)

The Coca-Cola Company is the biggest non-alcoholic beverage company in the world.

The company offers more than 500 brands across 200 countries and territories.

It has many iconic beverage brands under its umbrella that are sold around the globe.

The company has been a great investment over the long term, offering both capital appreciation and growing dividends.

Warren Buffett made it his largest holding in 1988 and it remains one of the biggest holdings for Berkshire Hathaway.

However, the last decade hasn’t been a good one for the company.

Compounded average growth rate(CAGR) of revenues over the last decade is just 0.6%.

Earnings per share CAGR over the same time period has been negative at -0.9%.

Free Cash Flow per share has grown at a CAGR pace of 2% over the last 10 years.

Although the company went through some business restructuring during that time period, the flat growth is not encouraging.

Let’s dig in to the details of this company.

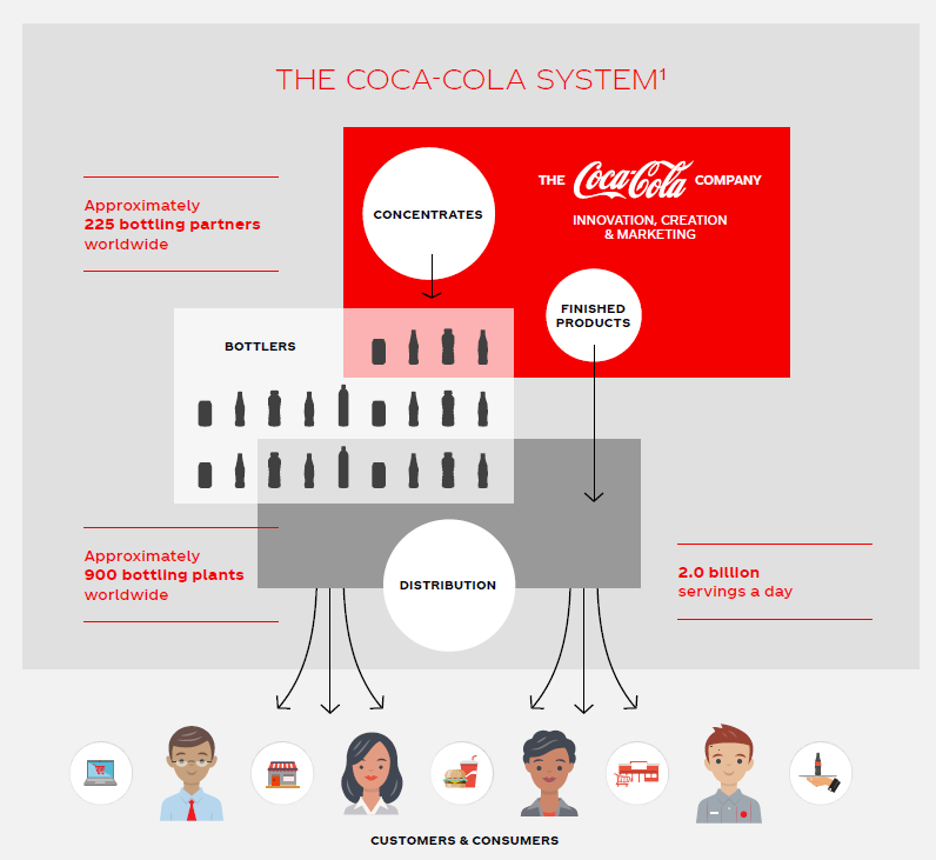

How does Coca-Cola make money?

When you think of Coke’s business, you probably think of shiny Coke bottles rolling off Coca-Cola’s production lines .

You will be surprised to know that this is not how The Coca-Cola Company makes most of its revenues.

Coca-Cola Company mostly sells the syrup concentrate for the soft drinks to local bottlers who are the regional franchisee. Those bottlers produce the drinks that you see on the shelves from the concentrate. Bottlers then sell the finished product to local restaurants, stores, food service distributors and vending machines.

The company has been actively selling its own bottling operations in a “refranchising” effort to become more asset-light. This has translated into lower total revenues for Coca-Cola, but higher margins.

Around 2/3 of KO revenues come from concentrate sales, with finished products making up the rest of the revenue mix.

Dividend

An impressive 57 years on consecutive dividend raises mean that KO is a Dividend King.

The company has rewarded long-term shareholders generously.

If you bought KO shares 30 years ago, you are doing very well.

Even without re-investing, the dividend income received from that investment would amount to almost 30% of the invested capital.

That’s the power of dividend growth.

For dividend investors today, KO doesn’t look as attractive.

Although it yields a solid 3.35%, the dividend growth has been slowing down.

The 5-yr CAGR growth is still above my minimum criteria of 5%, but the latest raise was just 2.5%.

At the same time, the FCF payout ratio has been climbing. Current dividend payments now make up almost 85% of 2019 FCF. This is very thin coverage.

Without free cash flow growth, the company can’t afford to significantly grow its dividend anymore.

| My Criteria | Coca-Cola | Pass | |

| Dividend Yield | >2% | 3.35% | Yes |

| Dividend Growth 5-yr CAGR | >5% | 5.6% | Yes |

| FCF Payout Ratio | <60% | 85% | No |

| Dividend Growth Streak | >5 years | 57 years | Yes |

Profitability

| My Criteria | Coca-Cola | Pass | |

| ROE | >12% | 29% | Yes |

| ROIC | >12% | 13% | Yes |

| FCF/Sales | >5% | 18% | Yes |

As we can see on the table above, Coca-Cola is a very profitable business. The strong brand name means KO can charge a premium for its products. KO itself doesn’t have to invest as heavily into assets, as bottlers take on that cost. That has helped Coke’s margins to improve and the company to be very profitable.

Balance Sheet

| My Criteria | Coca-Cola | Pass | |

| Debt/Equity | <0.5 | 1.7 | No |

| Debt/EBITDA | <3 | 3.5 | No |

| Interest Coverage | >8x | 14x | Yes |

Coca-Cola Company doesn’t fit my balance sheet criteria. However, as a defensive business, they can comfortably carry more debt on their balance sheet. It’s also important to keep in mind, that Coca-Cola has significant amounts of cash on its balance sheet.

In comparison to the total debt, KO has around 35% in cash.

They could significantly delever their balance sheet if they wanted to. However, as they can easily cover their interest expenses, there is no immediate need for that.

Valuation

| My Criteria | Coca-Cola | Pass | |

| P/E | <15 | 21 | No |

| P/FCF | <15 | 26 | No |

| CAPE | <20 | 26 | No |

In my opinion, Coca-Cola Company doesn’t warrant such an expensive valuation. The company is struggling to grow and its dividend coverage is becoming thin.

It seems that investors are bidding up KO’s stock as they see it as a “safe” pick. I don’t see flat business growth and a thinly covered dividend as “safe”.

Risks

In the short-term, the company’s franchisees will struggle from the reduced demand due to the coronavirus pandemic.

I don’t see it as a long-lasting threat, as economies around the globe are now opening up for business. However, Coke does rely on its franchisees being able to manage their own finances.

KO is a global brand with a long-lasting track record of profitability, but it is not untouchable.

The company has to keep up with consumer preferences. Consumers are gravitating more and more towards healthier options.

Coca-Cola is actively changing its product mix to keep up to date.

The company is doing it through acquisitions and developing new products itself.

Over the last decade, Coca-Cola Company has acquired businesses that offer a more “healthy” product. Those include brands such as SmartWater, Innocent, Appletiser, Zico, Fuzetea etc.

The legacy Coke drinks have also been re-developed to include less sugary options such as Coke Zero and Diet Coke. You can also see Coke in smaller cans now, to reduce the amount of sugar a customer consumes per can.

The stock price can also suffer from valuation risk.

If the company fails to re-ignite its growth, investors might not be willing to pay the current high multiple for it anymore. That might cause selling pressure and drive the price down.

Summary

I can understand the draw of KO for dividend investors. The company has proven to be a profitable business over a very long time frame and has an incredibly well-known brand name. Long-term shareholders have historically been handsomely rewarded for their investment.

But I don’t see KO as an attractive investment at this moment in time.

From a business perspective, it’s never good to see flat profits over a decade. Especially during a bull market.

Granted, the company is actively working to improve margins and manage their brand portfolio.

From a dividend growth perspective, I see very little room for the dividend to grow. As cash flows are relatively flat and the payout is in the mid-80’s, I don’t see much potential there.

Each investor should determine for themselves, if this company fits their investment goals and risk tolerance.

For me personally, I am “NEUTRAL” on this stock and don’t see it as an attractive income investment at this moment in time.

| My Criteria | Coca-Cola | Pass | |

| Dividend Yield | >2% | 3.35% | Yes |

| Dividend Growth 5-yr CAGR | >5% | 5.6% | Yes |

| FCF Payout Ratio | <60% | 85% | No |

| Dividend Growth Streak | >5 years | 57 years | Yes |

| ROE | >12% | 29% | Yes |

| ROIC | >12% | 13% | Yes |

| Debt/Equity | <0.5 | 1.7 | No |

| Debt/EBITDA | <3 | 3.5 | No |

| Interest Coverage | >8x | 14x | Yes |

| FCF/Sales | >5% | 18% | Yes |

| P/E | <15 | 21 | No |

| P/FCF | <15 | 26 | No |

| CAPE | <20 | 26 | No |

Coca-Cola Company scores 7 out of 13 on my checklist.

Disclaimer: I may hold positions in the companies mentioned. This is NOT an investing recommendation. You can lose your invested capital. I am not a financial professional of any kind. The article published should NOT be considered to be investing recommendation or basis for financial planning. Before making any investing or financial decisions, contact an appropriate professional. Figures used in this article are believed to be accurate, but shouldn’t be relied on for investing decisions. I am not responsible for the accuracy of the data presented. All content on this website is for entertainment purposes only.