This is the 3rd article in the dividend stock article series, where You have the power to decide the company I write about. The dividend-paying company that gets the most votes on my Instagram poll is the one I will write an article about. Today, in the third of the requested dividend stock article series, I am covering Procter&Gamble(PG).

Make sure to read the first requested article about Visa(V) here and the second article about AT&T(T) here.

The Requested Company

Procter&Gamble is a multinational consumer goods company headquartered in USA. The company has a wide portfolio of very well-known brands that are used by consumers around the globe in their everyday life.

How does Procter&Gamble make money?

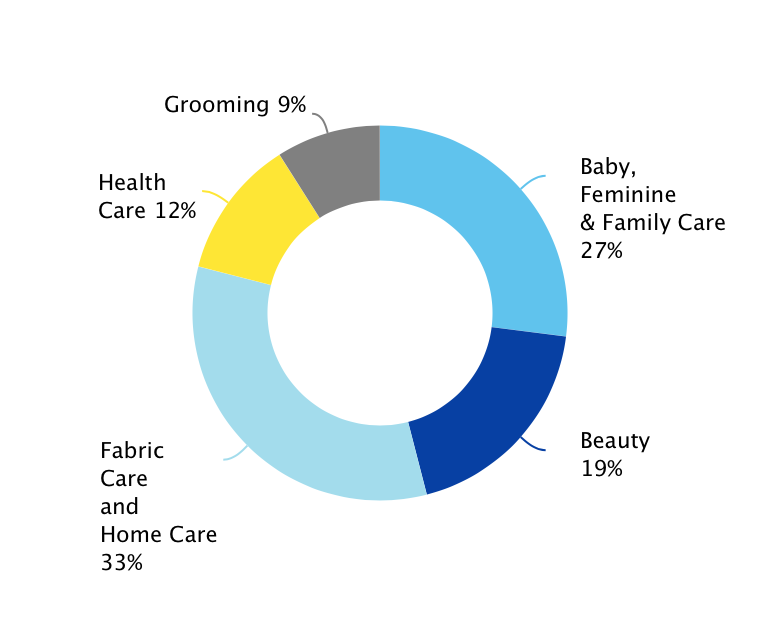

On the graph below are the 5 business segments represented as a % of yearly revenue.

Fabric & Home Care (33% of revenue) – Brands such as Ariel, Tide, Fairy, Febreze, Mr.Clean etc

Baby, Feminine & Family Care (27% of revenue) – Pampers, Always, Tampax, Bounty, Puffs etc

Beauty (19% of revenue) – Head&Shoulders, Herbal Essence, Pantene, Old Spice, Secret etc

Health Care (12% of revenue) – Oral-B, Crest, Pepto, Bismol, Vicks etc

Grooming (9% of revenue) – Braun, Gillette, Venus

You are likely familiar with many of the brands under the Proctor&Gamble umbrella.

Consumers are not likely to cut items such as toothpaste, razors, laundry detergent, shampoo etc from their budgets even if the economy takes a downturn. These are inexpensive items that people use in all economic conditions which makes P&G a non-cyclical company. Meaning that the demand for the company’s products remains strong at all times.

This is why investors view P&G as a defensive business to invest in.

Procter&Gamble Struggles

P&G has really struggled to grow during the last decade. Revenue, earnings and cash flow have been flat and even slightly negative over the last decade, emphasising the company’s inability to grow. On a per-share basis the company’s financials have improved, but that’s mostly due to buybacks. If the company is struggling to improve those metrics over the long run, it’s a very bad sign.

They have been actively trying to cut costs and divest some brands that are not performing well. Time will tell if that will help to re-vitalise the growth.

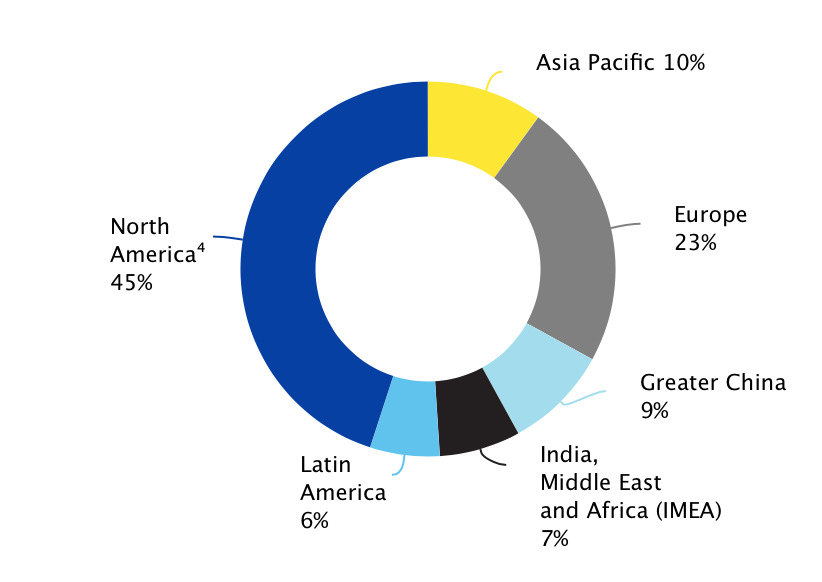

I believe, that the markets in which P&G operates has a lot to do with the slowdown. Below is the graph of revenues by geographic region.

As we can see, P&G’s revenues come mostly from more developed markets with older demographics. The demographics in emerging markets in comparison are much more favourable. The average age there is a lot lower and more people are entering the middle class. This means more potential new customers for consumer goods companies.

That’s one of the main reasons I personally prefer Unilever in the consumer defensive space. Unilever has around 60% of their revenues coming from emerging markets.

Dividend

The company’s dividend growth streak of 63 years of consecutive dividend raises is truly impressive. They have been able to grow the dividend throughout various crises and recessions. It also shows how they have been able to keep up with the times. Through acquisitions and rolling out new brands, the company has managed to keep up with consumers demands. The dividend streak of 63 consecutive years of raises is way above my minimum criteria of 5 years.

Investors that bought 30 years ago, are currently enjoying over 32% dividend yield on their initial investment. This is the power of dividend growth over the long-term.

Current dividend yield is 2.73% which is higher than my minimum requirement of 2%.

However, the dividend growth has slowed down lately, as the company’s growth has stalled. The 5-yr CAGR dividend growth rate has been just 3.13%, which is too low by my minimum criteria of 5%. Combine that with the starting yield, it’s not a very attractive income investment for me.

Next, I want to look at how big of a % of FCF is the company paying out as dividends. Using the 2019 FCF, the current dividend makes up 66% of FCF. That is too high my by criteria. I look for dividend investments with a FCF payout ratio of below 60%.

As the company has struggled to grow cash flows, the dividend raises have been possible by increasing the payout ratio. There is only so much you can raise dividends this way, without putting the dividend at risk.

P&G scores 2 out of 4 on my dividend criteria.

Profitability

Over the last decade, the average ROE was 17%. I look for ROE >12% so P&G is doing well in that area.

ROIC was 11.5% on average during the same period. That is just below my ROIC criteria of >12%.

My criteria when analysing companies using FCF/Sales is >5%.

Procter&Gamble passes this test with ease, with FCF/Sales at 14.6% on average over the last decade.

P&G scores 2 out of 3 on my profitability metrics.

Balance Sheet

Debt/Equity stands at 0.52 , which is just above my max 0.5 criteria.

Debt/EBITDA is currently 3.35 , slightly too high by my max criteria of 3.

Interest Coverage is a very safe 18x, comfortably higher than my criteria of minimum 8x coverage.

P&G’s balance sheet scores 1 out of 3 on my criteria.

On first glance it might seem that P&G has a lot of leverage as it doesn’t pass a lot of my criteria. It’s important to bear in mind though, that in consumer defensive space companies tend to have more debt. It’s because their earnings are more predictable as they sell things that are in demand throughout an economic cycle. That allows them to use more debt. They are less likely to see a sharp drop in their cash flows that would reduce their ability to service their loans. I don’t have any immediate concerns about P&G’s debt levels.

Valuation

I’m surprised to see P&G trading at such expensive valuations.

P/E of 22 is too high by my P/E criteria of 15.

P/FCF of 22 is above my threshold of 15.

CAPE Ratio currently stands at 29, too high by my criteria of 20.

I don’t see the benefit of paying such a high multiple for a company that is not showing any organic growth.

Although the demand for P&G products is likely to remain strong in all economic conditions, this doesn’t warrant such a high multiple in my opinion.

Valuation score for P&G is 0 out of 3.

Summary

P&G is a company that has rewarded shareholders through growing dividends for a long time. Many investors see the long track record and the defensive nature of the business and immediately see it as a good investment regardless of the fundamentals.

I disagree.

In my opinion, the company is not looking like a good dividend investment right now.

This is due to the combination of a decade of NO growth, current high valuations and little room for the 2.73% yielding dividend to grow.

Granted, the dividend is likely to stay safe for the foreseeable future. If you have been invested in P&G over a long timeframe and have a high Yield-on-Cost, it’s a different situation. I don’t see P&G as an attractive dividend growth investment going forward for new investors though.

P&G scores just 5 out of 13 on the metrics I use to analyse dividend investments.

Hope you enjoyed reading the 3rd requested dividend stock article on Procter&Gamble(PG)!

Disclaimer: I may hold positions in the companies mentioned. This is NOT an investing recommendation. You can lose your invested capital. I am not a financial professional of any kind. The article published should NOT be considered to be investing recommendation or basis for financial planning. Before making any investing or financial decisions, contact an appropriate professional. All content on this website is for entertainment purposes only.