Quick Thesis:

-

- Small-cap, triple-net lease REIT serving a fast-growing industry

-

- 15-yr average leases with yearly rent increases

-

- Very high cap rates significantly boost growth

-

- 100% occupancy since inception

-

- No net debt on its balance sheet

-

- Trading at a large discount to industry peers

The Company&Full Thesis

NewLake Capital Partners(NLCP) is a triple-net lease REIT providing real estate for U.S, state-licensed cannabis operators.

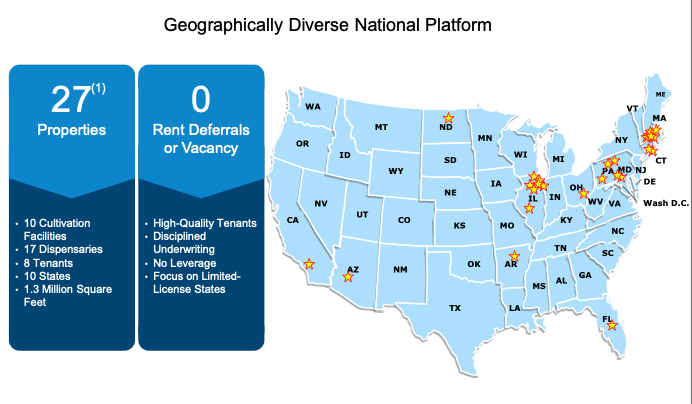

The company acquires properties from U.S based multi-state cannabis operators and leases them back on long-term net-lease deals. Those properties are diversified across the cannabis supply chain: cultivation facilities, dispensaries, logistics – and manufacturing facilities. The current portfolio consists of 27 properties comprising of 1.3 million sq feet of real estate leased out to 8 tenants in 10 states.

The average lease term is around 15 years, with the built-in lease escalators increasing yearly rents by 2.5% on average. This creates highly robust cash flows with some built-in inflation protection. 2.5% might not seem that much, but as the leases are so long, it would require many years of above-average inflation for the company to feel the pinch of higher inflation eating into the rent growth.

NLCP’s tenants are some of the leading operators in the U.S cannabis sector, such as Trulieve, Curalief, Cresco Labs and Columbia Care. The company has said that the tenants rent coverage is on average around 4-6x EBITDA which means that the tenants can comfortably cover their rent payments through business proceeds.

Thanks to a careful underwriting&tenant vetting process, the REIT managed a 100% occupation for a long time. Rent collections were also stellar until a rent collection issue arose at the end of 2022 with 2 tenants (Rev. Clinics now in receivership and Calipso)

The Cannabis Opportunity

Seventeen states in the U.S have legalised the use of recreational marijuana. That means 43% of the total U.S population now live in the states that have legalised the use of cannabis. According to a 2019 study, 18% of U.S adults say they have used cannabis in the last year, with 11% using it in the last month.

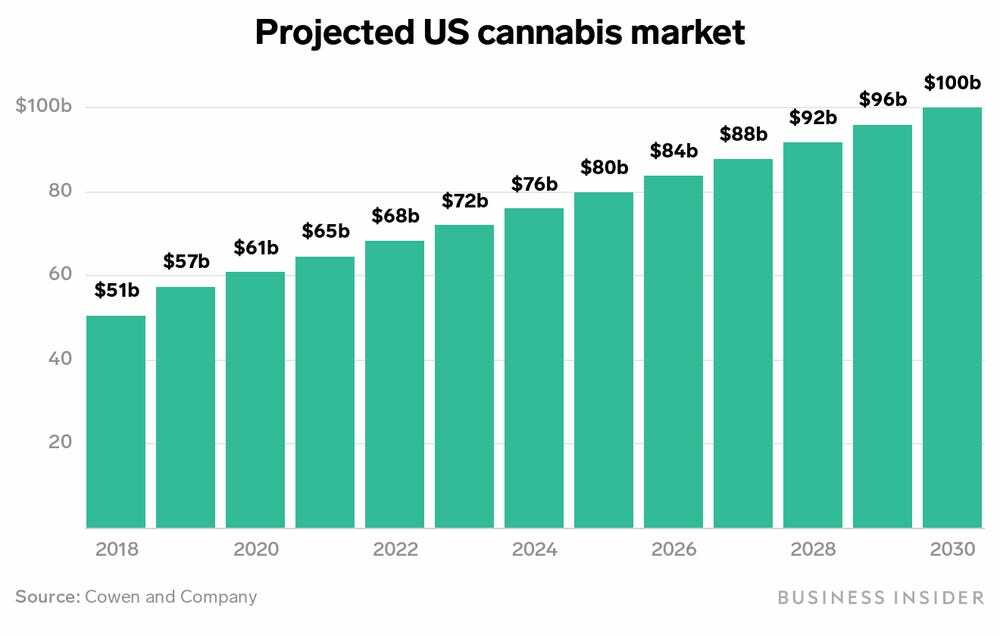

Cannabis sales are expected to grow from $13.4B in 2020 to a whopping $33.6B by 2025, representing 20% compounded annual growth and the projected U.S cannabis market worth by 2030 is estimated to be at $100B.

However, as the laws still vary greatly between state and federal levels, it’s hard for the cannabis operators to get access to traditional funding methods.

This is where cannabis REITs such as NLCP come in.

They acquire properties from the operators (freeing up capital for operators) and lease them back on extremely high cap rate, long-term, net-lease deals.

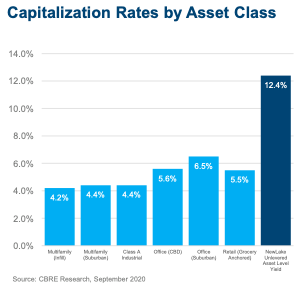

NLCP is able to lease out properties on 11-13% cap rates, which is extremely lucrative.

You can see on the chart below how favourably that compares to other real estate classes.

NewLake has openly admitted that they are emulating the business model of the first U.S cannabis REIT – IIPR . IIPR was the first-mover in this sector, and it has been on of the best-performing REITs of the last 5 years. Due to the smaller size, NLCP is currently flying under the radar, but if it manages to emulate IIPR’s success – it’s potentially an interesting opportunity.

Dividend

The company only recently initiated the dividend. But it’s clear that they are committed to growing it, with regular increases.

As the CIO Anthony Coniglio said: ” We purchase properties, we collect rent and we distribute a nice, healthy quarterly dividend to our shareholders”

At the time of writing, that represents a 12% forward dividend yield, with latest raise coming in at +2.5%.

Based on annualised aFFO estimate, the AFFO dividend payout ratio is around 84%.

I’m not expecting much growth from the dividend but the re-investment of that high yield will be a very strong growth lever for investors.

Balance Sheet

NLCP has one of the lowest debt levels in all of REITdom, with no net debt on the balance sheet (gross debt/EBITDA around 0.2x)

Valuation

I’ll be using 2 methods to determine FV for NLCP.

Dividend discount model with 10% discount rate and 2% growth rate gives us a FV target of $17.2 per share

Due to the industry specific-risk and recent rent collection issues I’m applying a 10x Fair Value aFFO multiple to NLCP.

Applying a 10x multiple to yearly aFFO gives us a Fair Value target of $20.1 per share.

Average of the 2 methods comes out to $18.65 per share.

Fair Value was updated after Q1 2025 earnings

Risks

Very concentrated portfolio with 45% of base rent from just 2 tenants.

Immediate risk concerns Revolutionary Clinics- a tenant that is struggling and is struggling to make rent payments. It’s rent payments make up 10% of NLCP revenues so the risk is significant if RC fails to improve its cash flow situation.

There is currently a large disconnect between state and federal laws regarding cannabis in the U.S. That has created the opportunity for companies like NLCP to invest and lease out properties to the industry at an extremely lucrative cap rates, as traditional financial institutions are not offering their services to the cannabis industry. As banks won’t lend to cannabis operators, they are turning to the NLCP’s for sale-leaseback transactions and other ways of funding. In a sale-leaseback transaction, the operator sells their property to the REIT and the REIT immediately leases it back to them on a long, net-lease contract. Something like selling your house and renting it from the person you sold it to. It frees up capital for the operators.

If federal and state laws would align, it would bring a lot of new capital into the cannabis sector. Operators could get loans from banks etc which would reduce the need for those sale-leaseback transactions. As a whole – it would significantly compress cap rates for cannabis REITs. For future transactions it would limit the REIT growth, but as the CIO/President of NLCP said in this interview, it would also benefit them. The cash flows of the operators would improve/stabilise and NLCP would also get access to cheaper capital – meaning that as cap rates decrease, the cost of capital comes down as well – allowing the company to potentially maintain similar spread between the 2 as they do now.

66% of capital invested by NLCP has gone into deals with 4 tenants, meaning that it’s not yet as diversified as some of its bigger peers. As the company is still growing, there is plenty of runway to improve diversification.

As there is ample demand for cannabis-related real estate, the company shouldn’t have too much trouble finding a new tenant, if one were to default on the lease deal or go out of business. For example in Illinois, the state received around 700 applicants wanting to open a dispensary but only 75 licences were granted. In some states the operator has to have a property in place before applying for the license, which also creates increased demand for those spaces.

In my opinion, the entry of banks into this market is still years away. Banking is such a tightly regulated industry and banks would have to navigate very complex (and currently unclear) compliance measures in order to invest there.

Summary

NewLake Capital Partners gives investors a unique opportunity to invest in a rapidly-growing sector through a profitable and dividend-paying entity. With a diversified base of carefully vetted multi-state tenants, the company has managed to achieve a 100% occupation rate and recently got back to 100% rent collection. Also the balance sheet is debt-free and the company is significantly discounted compared to peers. I am bullish on the potential of this dividend investment.