To see the stocks that I rate higher than Caterpillar, check out the Premium Membership

I’m always curious to know which stocks other dividend growth investors are following and researching. So, I ask people who follow me to choose the stocks they want me to write about. Today, I’m bringing you the latest requested analysis article – Caterpillar(CAT) . Keep an eye on my Instagram page to vote and find out which company I’ll look at next in this series.

The Company

Caterpillar(CAT) is a global leader in the construction and mining equipment industry. Founded in 1925, the company has grown to become a Fortune 100 powerhouse, thanks to its diverse range of products and services that cater to various industries, including construction, mining, energy, transportation, and agriculture.

The company primarily generates its revenues through the sale of machinery and engines.

- Machinery segment: construction, mining, and forestry equipment.

- Engines segment: diesel, natural gas, and industrial gas turbines.

CAT’s business model relies heavily on its extensive, global dealer network. This network comprises over 160 independent dealers, operating in more than 190 countries and territories. The majority of these dealers exclusively sell Caterpillar products, giving the company a competitive edge in the market.

Caterpillar’s products can be described as “high-end” since the price tag for the heavy equipment is very high. However, customers in those industries are not only looking at the initial price but also the “lifetime cost” of the equipment – including maintenance and repair costs, costs for spare parts, fuel costs etc. Adding all those up, Caterpillar compares favourably to peers and is one of the reasons that Caterpillar is the market leader in those segments.

The main catalysts for demand in the near future is the U.S infrastructure bill which will drive massive spending on repairing and improving infrastructure in the U.S. However, large capital investments are also quite cyclical and depend on the health of the overall economy. As Caterpillar operates in a cyclical industry, its operational performance ebbs and flows with the strength of the underlying economy.

10-yr performance:

- Revenue per share CAGR +0.8%

- EPS per share CAGR +3.5%

- FCF per share CAGR +8.6%

Dividend

Caterpillar has achieved the much-coveted Dividend Aristocrat status by raising the dividend for 29 consecutive years.

For a cyclical business that is a truly impressive feat.

At the time of writing, shares of CAT offer a 2.2% forward dividend yield that is covered with a 47% free cash flow payout ratio.

The dividend growth can be quite “lumpy” with some huge raises at cycle highs and low single-digit raises in other periods, but over the last decade the dividend has grown at a CAGR of just below 9% with the latest raise in 2022 at 8%.

The company also runs a share repurchase program, with an average of 3.6% of the float per year bought back over the last 5 years.

Balance Sheet

Caterpillar has an A rated balance sheet (S&P, Moody’s).

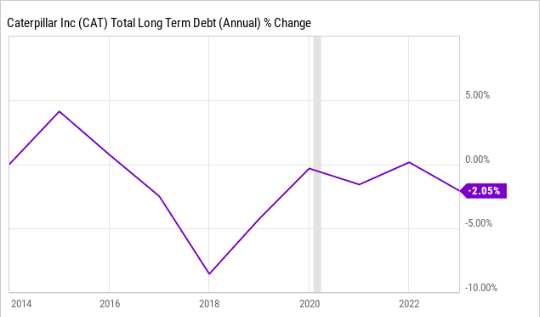

But for a cyclical company, it does carry quite a bit of debt on its balance sheet in comparison to its profits.

Debt/EBITDA ratio stands at 3.2x, which is higher than I’d like to see for an industrial company. However, as we can see on the graph below, total debt load has been very steady over the last decade.

The company is also very comfortably financing its debt obligations, with interest payments covered 20x over by yearly EBIT.

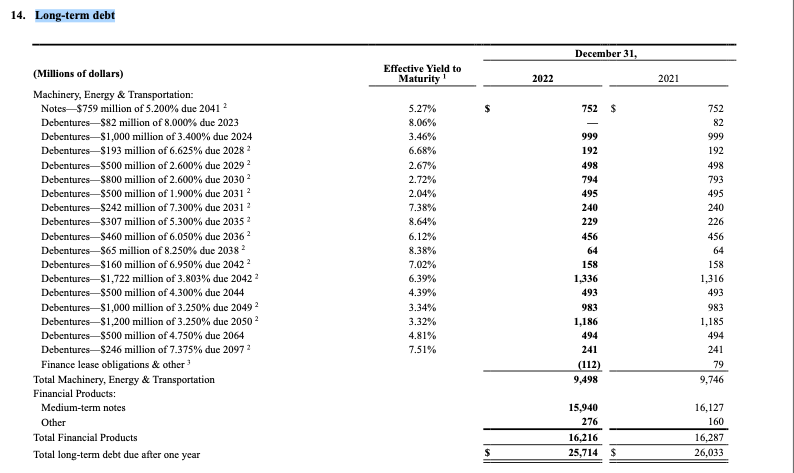

Looking at the debt maturities, we can see that CAT has quite a lot of debt maturing in 2024, which will be likely re-financed at a higher rate but overall the credit markets seem confident in Caterpillar’s prospects and the company is unlikely to run into liquidity or re-financing issues.

Valuation

Analysts seem very confident on CAT’s earnings potential over the next few years, with consensus suggesting +15% EPS growth in 2023 and +7-8% growth in 2024/25. With recession signals flashing red, I’m a lot more cautious about Caterpillar’s earnings growth over the next few years due to its cyclicality. But over the full cycle I do believe a high single-digit FCF growth rate is feasible.

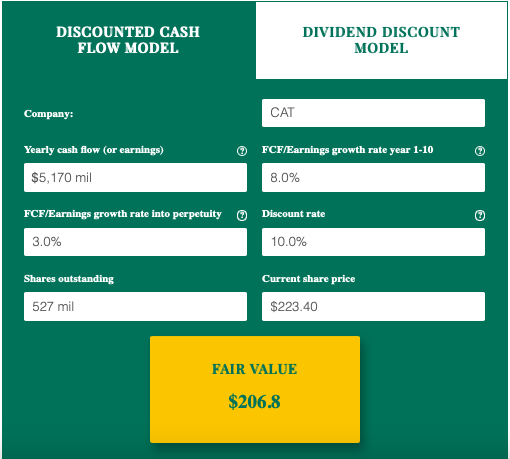

Running a 2-stage Discounted Cash Flow Model with +8% FCF growth over the next decade and a 3% perpetuity growth rate discounted at 10% gives me a Fair Value target of $206.8 per share suggesting that shares are currently overvalued.

Other valuation metrics suggest the same.

Shiller P/E or CAPE ratio (cyclically adjusted P/E ratio) stands at 29x suggesting that on a cycle-average basis shares are trading at a very high multiple. CAPE ratio is an useful tool for valuing companies with cyclical cash flows.

If we also include debt levels into the equation and look at it through an EV/FCF (Enterprise Value/Free Cash Flow) lense – shares are also looking expensive at a 28x multiple.

Risks

Caterpillar’s operational performance is highly correlated with global economic cycles. A downturn in the economy could significantly impact the company’s revenues and profitability.

As the company operates in a highly globalized market, it is subject to geopolitical tensions and trade disputes, which could adversely affect its business. USA-China tensions are the most prevalent geopolitical risk for industrials currently.

As a multinational corporation, Caterpillar is exposed to currency fluctuations, which can impact its financial results.

Operations are subject to various regulations and environmental standards, which can change over time and increase costs or limit growth opportunities.

Caterpillar faces intense competition from both established rivals such as Komatsu and emerging technologies, which could threaten its market position.

As the company relies on its dealer network, any disruptions or issues within this network could negatively affect the company’s performance.

Summary

Caterpillar is undoubtedly a high-quality business with a strong competitive advantage. However, its current valuation may not accurately reflect the potential challenges and risks it faces in the coming years. As a result, I’m looking at other investment opportunities that offer a more favorable risk-reward profile.

At current valuation it’s a “HOLD” rating from me.

To see the stocks that I rate higher than Caterpillar, check out the Premium Membership