As voted by my Instagram followers, I bring You the requested dividend stock analysis article on 3M(MMM)

If you are interested in my investments, check out the template I used for creating my investing plan.

The Company

3M(MMM) is an American conglomerate. It has global operations and a very diversified business, selling more than 60,000 products all over the world.

The company operates in 4 main business segments.

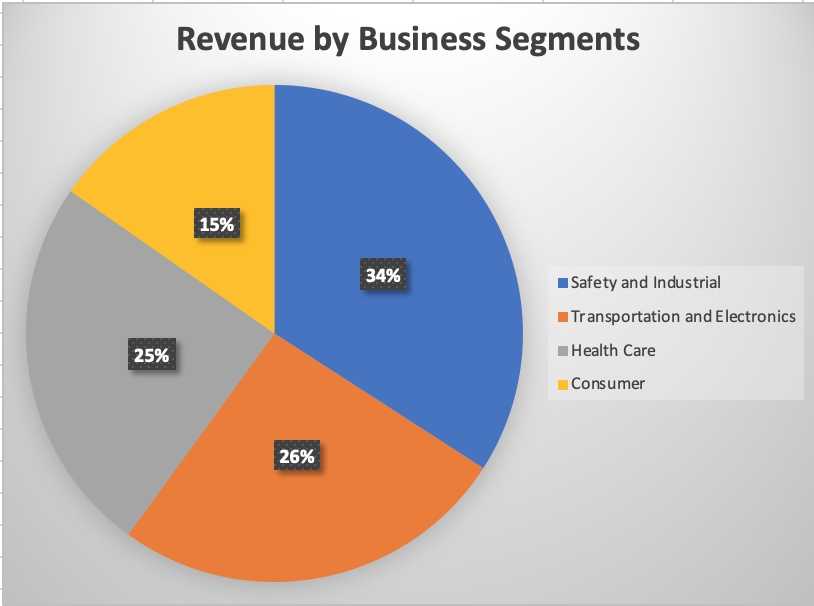

- Safety and Industrial – Building safety solutions, hearing&eye&respiratory protection solutions, industrial abrasives, autobody repair solutions, structural adhesives&tapes, cable accessories etc

- Transportation and Electronics – Display enhancement films, auto electrification solutions, reflective signage for highways and construction safety, sound and temperature management, electronic assembly solutions, large format graphic signs for adverts etc

- Health Care – Drug delivery, dentistry, skin&wound care, infection prevention, filtration&purification systems etc

- Consumer – Retail abrasives, paint accessories, DIY car care, consumer air quality solutions, home cleaning products, consumer bandages&braces etc

Below is the total revenue (per latest earnings report) divided across the 4 segments.

As we can see, 3M’s sales are well-diversified across segments.

In addition to this, revenue is also diversified across regions with 3M selling its products globally.

3M Dividend Analysis

3M is a truly iconic dividend growth stock. It has raised its dividend for 62 consecutive years now, with long-term holders enjoying extremely high yield-on-cost.

For investors who bought 3M shares 30 years ago – their yield-on-cost is over 26% per year (without re-investment). That shows the power of long-term dividend growth investing.

The current yield is 3.7%.

As 3M has pulled 2020 guidance, I used 2019 figures to evaluate dividend safety.

Based on 2019 figures, the dividend is covered with a 64% FCF payout ratio and 74% earnings payout ratio.

Over the last decade, the dividend grew at a very impressive 11% CAGR pace. However, a significant portion of that came from raising the payout ratio.

The earnings payout ratio was 37% in 2010 – it has increased up to 67% by 2019.

It benefited shareholders as their income grew.

But that dividend growth lever has now been used up. The company has to grow its earnings and cash flows to fund the dividend raises now.

That has caused the dividend growth to slow down.

The latest dividend raise was just 2%.

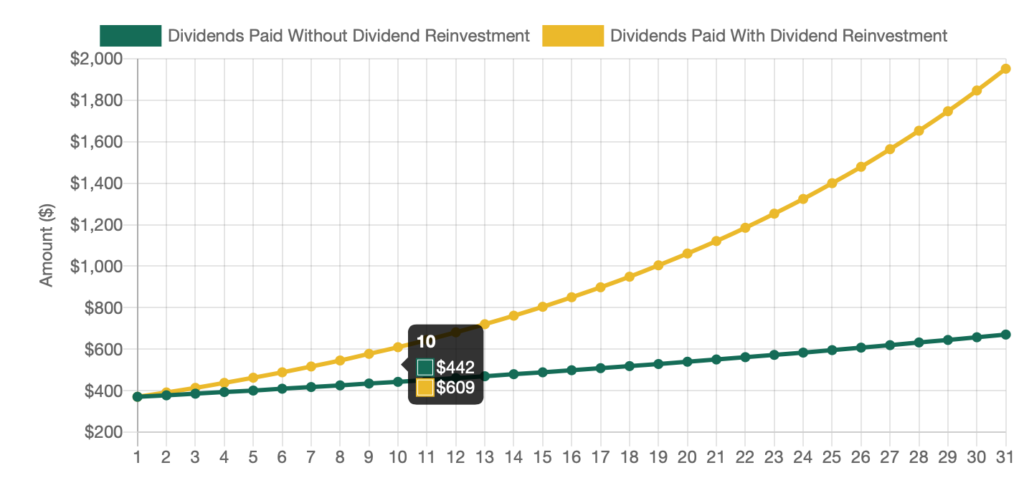

I ran the current yield and the latest raise by my Dividend Growth Calculator. This gives me a rough estimate of the future income I might expect from 3M.

As seen on the graph above, through dividend raises and dividend re-investing, I estimate around 6% of income from current investment in 3M in 10 years time.

It’s not explosive dividend growth, but 3M‘s dividend remains safe.

Profitability

This conglomerate is a very profitable enterprise.

It passes all 3 profitability criteria that I use in my analysis.

Return on Equity (ROE) is 50%, although this number has been distorted by debt-funded buybacks reducing shareholders equity.

Return on Invested Capital stands at 17% based on trailing twelve months figures.

FCF/Sales is currently 17%. This means 3M has 17% of cash left over from each sale, after accounting for the expenses of running the business.

Balance Sheet

As many other large companies have done, 3M has significantly increased its leverage as it can borrow at very low rates in current environment.

Long-term debt alone doubled between 2015 and 2019.

Debt/Equity is 1.96 and has increased meaningfully from 0.27 levels in 2010. The company has been making use of low interest rates and funded buybacks with increased borrowings.

Debt/EBITDA is 2.8, which is a safe level for this company.

Interest payments are very safely covered 14x over from annualised EBIT.

Although interest payments remain safely covered, the coverage has been trending downwards. For comparison, in 2015, interest coverage was 43x.

3M has been able to borrow at very low interest rates. In Q1 of 2020, the company borrowed $1.75 billion at a weighted average rate of just 3.2%.

The company has the capacity to borrow another $4.25 billion from its revolving credit facility, if needed.

Valuation

Identifying a great company is only half of my investment process.

Buying, when shares are trading at attractive valuations is equally important.

3M is a dividend king that has been growing its revenues and cash flows over a long time frame. The company remains in a good position to continue rewarding shareholders with dividends.

However, valuations are currently elevated for a slow-growing company.

3M stock is currently trading at just under 20x forward earnings.

P/FCF is currently 17, and the CAPE ratio is just over 20.

Per my personal investment criteria, 3M shares are currently overvalued.

Risks

Increased leverage to fund buybacks and elevated dividend payout ratio are the biggest risks to the dividend. Although I expect the company to keep paying out dividends, the potential for dividend growth is much lower now.

Lawsuits are another potential risk to the business and 3M‘s reputation.

For example, the whistleblower lawsuit in 2016, claiming 3M was knowingly selling defective earplugs that were used by the US military

In 2018 the company agreed to pay $9.1 million to the US government to resolve the case without admitting liability. Since 2018, more than 140,000 former users of the product (mostly military veterans) have filed lawsuits against 3M.

Summary

3M has been a cornerstone holding for many dividend growth investors. It has delivered 62 years of consecutive dividend raises and has a diversified, profitable business.

From a dividend growth perspective, I see limited upside to the dividend from current levels. As a result of the increased debt levels and the elevated payout ratio, the potential for dividend growth is limited.

Combined with the current high valuation, I don’t currently see 3M as an attractive dividend investment for my personal portfolio.

3M scores 8 out of 13 on my investment criteria checklist.

| 3M | My Criteria | Pass | |

| Dividend Yield | >2% | 3.75% | Yes |

| Dividend Growth 5-yr CAGR | >5% | 11% | Yes |

| FCF Payout Ratio | <60% | 64% | No |

| Dividend Growth Streak | >5 yrs | 62 yrs | Yes |

| ROE | >12% | 50% | Yes |

| ROIC | >12% | 17% | Yes |

| FCF/Sales | >5% | 17% | Yes |

| Debt/Equity | <0.5 | 1.96 | No |

| Debt/EBITDA | <3 | 2.8 | Yes |

| Interest Coverage | >8x | 14x | Yes |

| P/E | <15 | 19.7 | No |

| P/FCF | <15 | 16.7 | No |

| CAPE | <20 | 20.3 | No |

Disclaimer: I may hold, initiate or trade positions in the companies mentioned. This is NOT an investing recommendation. You can lose your invested capital. I am not a financial professional of any kind. The article published should NOT be considered to be investing recommendation or basis for financial planning. Before making any investing or financial decisions, contact an appropriate professional. Figures used in this article are believed to be accurate, but shouldn’t be relied on for investing decisions. I am not responsible for the accuracy of the data presented. All content on this website is for entertainment purposes only.