Developing a Dividend Investment Plan

Building a dividend growth portfolio tailored to your retirement income needs requires careful planning. By evaluating your income requirements, selecting the investments with the necessary yields and dividend growth rates, you can create a portfolio that you can retire on and rely upon in any stock market conditions.

- Evaluating Your Requirements

Before you start building your dividend portfolio, you have to establish what does dividend investing success look like for you. For that we need to determine your income needs during retirement. Consider the following steps:

- Calculate your expected monthly expenses during retirement, including housing, food, healthcare, and other various expenses.

- Determine any other sources of income you’ll have during retirement, such as Social Security, pensions, or part-time work.

- Subtract your other income sources from your monthly expenses to find the amount you’ll need from your dividend portfolio.

- Adjust the required income for inflation using this calculator.

- Determine your investment time horizon – when do you want to achieve your goals by.

O

Luckily -our Dividend Investing Calculator does all the heavy lifting for us and allows us to figure out the portfolio average yield and dividend growth rate needed to achieve our financial goals.

2. Selecting the Stocks That Fit Your Goals

In the previous lessons we’ve already learned how to assess a potential investment via various fundamental metrics.

Once you know your goals and have calculated the required avg. portfolio yield and growth rate required for it – it’s time to pick the stocks that will get you there.

While first and foremost it’s crucial to look at the quality of the underlying business – we will be further filtering it down per yield and dividend growth to come up with the stocks that fit our personalised goals.

I prefer a mix of higher-yielding and lower-yielding stocks with correspondingly lower and higher growth potentials to achieve the average yield+growth required.

Higher-yielding stocks provide more compounding via re-investing whilst lower-yielding, higher-growing stocks provide organic growth.

It’s important to achieve a good balance between both.

When still accumulating, the re-investment of dividends will do most of the lifting but once you start living off the dividends, organic dividend growth via dividend raises will be the only way your income grows.

Once retired – organic dividend growth is our protection against inflation.

The important metric to track is Yield-on-Cost

Yield on cost (YOC) is a measure used by dividend investors to track the power of dividend growth and re-investment in relation to their original investment. It’s calculated by dividing the annual dividend paid by the security by the original cost basis of the investment. For example, if you receive a $9 annual dividend for every $100 you originally invested in a stock, your yield on cost would be 9%.

Unlike dividend yield, which shows how much dividend income every dollar invested at a stock’s current price will produce, YOC focuses on the dividends received relative to the initial investment. Yield on cost increases when a company raises its dividend and decreases when a company cuts its dividend.

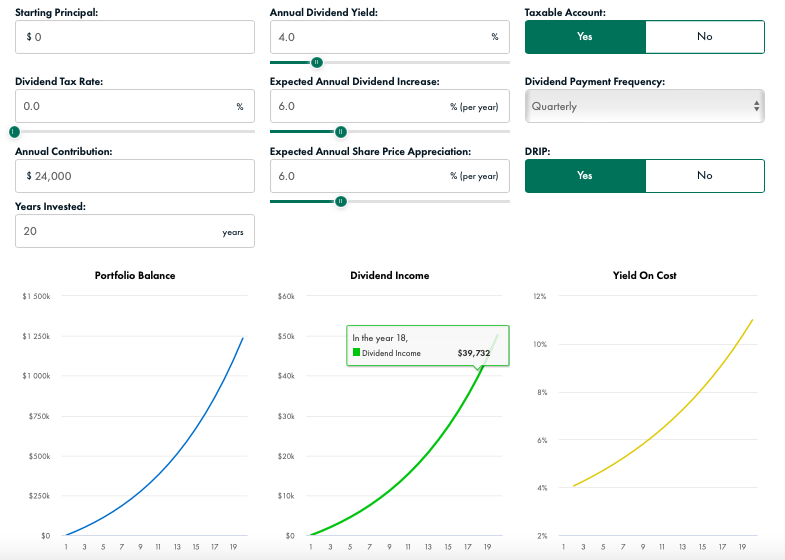

Example using our built-in Dividend Investing Calculator

An investor starting from $0 invested and wanting to reach a yearly dividend income of $40,000 would need to invest $2000/month for 18years (and re-invest all dividends along the way and assuming share price growing in-line with dividend) to reach that goal.

You can play around with different $ amounts, dividend yields and growth rates in the Dividend Investing Calculator to see what it takes to reach a certain goal.