With the stock markets hitting all-time highs, it's hard for investors to find undervalued stocks. As the rising tide lifts all boats, so has the broader market boosted the stock prices of most companies.

At the time of writing, the S&P500 is trading at a P/E ratio of 37. That's well above the S&P's historical median valuation of just under 15x earnings.

Whilst many new investors have developed the mantra of "stocks always go up", that's not always the case. There has been many periods historically, where buying overvalued stocks has resulted in terrible returns for a decade or even longer. Even when buying quality companies.

Identifying a great company is only one side of successful investing - buying at the right valuation is equally important.

We only have to look at the second largest company on the S&P500 - Microsoft, for a great example.

It's a fantastic business that has consistently grown its earnings over a long time period.

However, if you bought MSFT shares in 1999, when the stock valuation was very high - it took you more than 15 years to break even!

Even though the business kept performing well, buying at overvalued levels turned out to be a poor investment.

Therefore my investment plan is simple- buy great dividend-paying companies, when shares are trading at an attractive valuation.

Today's post outlines 2 most undervalued dividend stocks in my opinion. These companies are performing well as a business and rewarding shareholders richly through growing dividends. However, they are currently very much out of favour and the valuations reflect that. For a contrarian investor, they provide a potentially interesting value proposition.

The 2 Most Undervalued Stocks

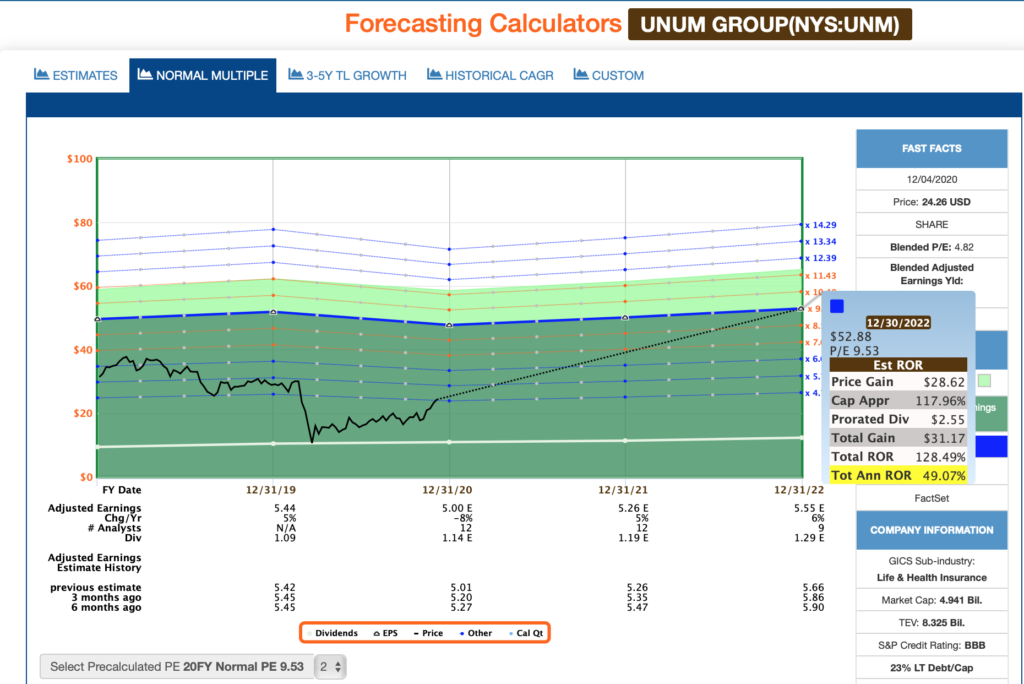

#1 most undervalued stock - Unum Group(UNM)

Unum Group(UNM) provides group and individual insurance products in the U.S, UK and Poland. The majority of insurance premiums are generated from employers plans.

At the time of writing, shares of UNM are trading at a bargain P/E valuation of <5.

For such a low P/E ratio, you would think that Unum Group was a company hovering on the brink of bankruptcy.

In reality, Unum Group has grown its earnings per share every year since 2005 and pays a well-covered dividend . Analysts expect this insurance company's earnings to decline by -8% in 2020 before resuming EPS growth in 2021 and '22.

Unum is currently paying a 5.2% dividend that is covered with an extremely safe earnings payout ratio of just 20%. Unum's business could take a significant hit and still be able to afford the dividend.

Looking at the F.A.S.T Graph below, if shares of UNM were to revert to their 20-yr historical average valuation of ~9.5 blended P/E by 2022, the total annualised return would be a whopping 49%.

There is no guarantee that the market will realise Unum's solid business performance by then, but investors can collect the solid, growing dividend in the meantime.

Risks

The current low interest rate environment is not ideal for insurance companies. As they invest their float largely into bonds and hold them until maturity, it's currently tough to find investment-grade bonds with significant income potential. Insurance companies have to adapt to this situation. Investing the float is only one part of insurance company earnings however, as they generate profits from the insurance premiums.

The long-term care policy segment carries with itself a potential risk. Unum stopped offering those policies in 2011, but they still carry some on their books from time prior to that. There is a possibility that the company will have to increase their LTC reserves significantly, with Credit Suisse estimating a $5.7 billion deficit last year.

The company is actively managing this, but it remains a potential risk until those policies expire.

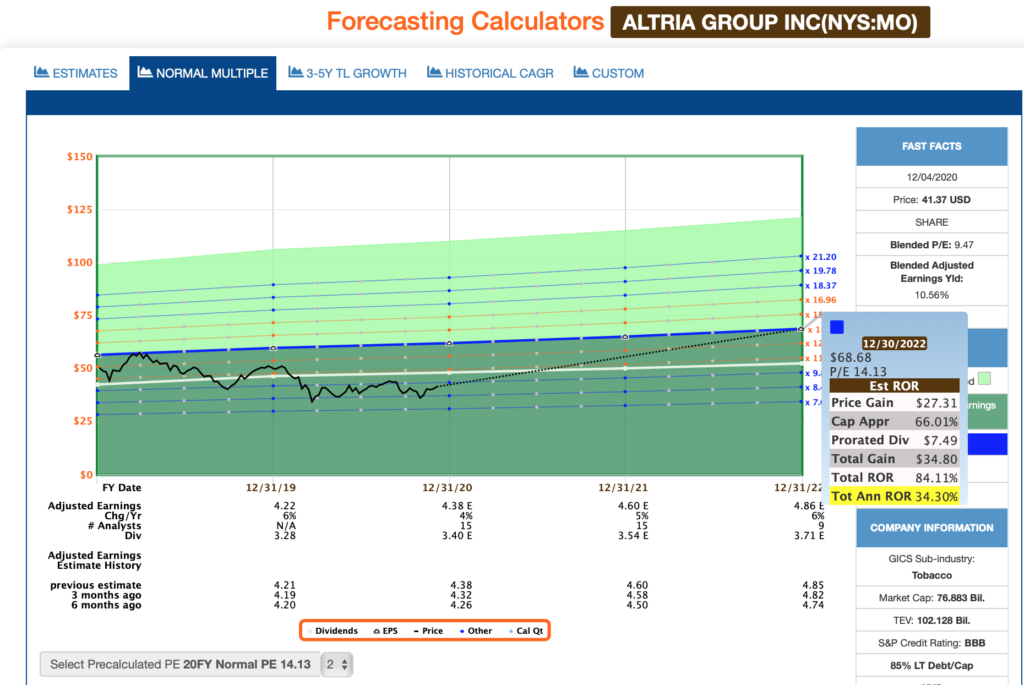

#2 most undervalued stock - Altria(MO)

Altria(MO) is one of the world's largest producers of tobacco and cigarettes. The cigarette business is certainly in decline, but it's still very cash flow generative for the company as the company has strong pricing power and customers show great brand loyalty. The cash flow is directed into paying the dividend and developing new tobacco alternatives to cigarettes.

The company is currently not getting any credit for its solid business performance as shares are trading at a blended P/E valuation of 9.5.

Although the traditional cigarette business is facing long-term headwinds, the company has performed extremely well.

EPS has grown every single year since 2004 and this year is no exception. Altria is estimated to grow its EPS by 4% in 2020 in spite of difficult conditions.

Today's investors are getting a 8% yielding dividend.

Earnings payout ratio of 78% is just below the company's adjusted diluted EPS payout target of 80%.

Looking at the F.A.S.T Graph below, we can see that if shares were to revert to their 20-yr historic average blended valuation in 2022, the potential total return would be in excess of 34%.

Of course there is no guarantee that the market would re-assign a higher multiple to Altria's shares, but investors can currently lock in an extremely high yield of 8.3%.

Risks

Tobacco industry is very heavily taxed, regulated and unpopular on the Wall Street.

Amount of cigarette smokers is certainly declining - and that's a great thing. The company is not fighting against the trend, but rather proactively developing non-combustible tobacco products and converting adult smokers to those products. Those products include for example nicotine gums, tobacco pouches and electronic cigarettes.

There is however significant execution risk for transitioning from transitional cigarettes to new alternatives. Additionally, the company faces many new competitors in the alternative tobacco space.

Summary

In current overvalued market conditions, value-conscious investors could do a lot worse than looking into those 2 most undervalued stocks. They show growing earnings and dividends in spite of being largely ignored by the market.

Disclaimer: This is NOT a recommendation to buy or sell any shares. You can lose a part of or all your invested capital. I am not responsible for the accuracy of any of the figures presented in the article. I am not a financial professional of any kind. Any stock transactions or analysis published should NOT be considered to be investing recommendations. Before making any investing or financial decisions, contact an appropriate professional.This website should be viewed for entertainment purposes only.